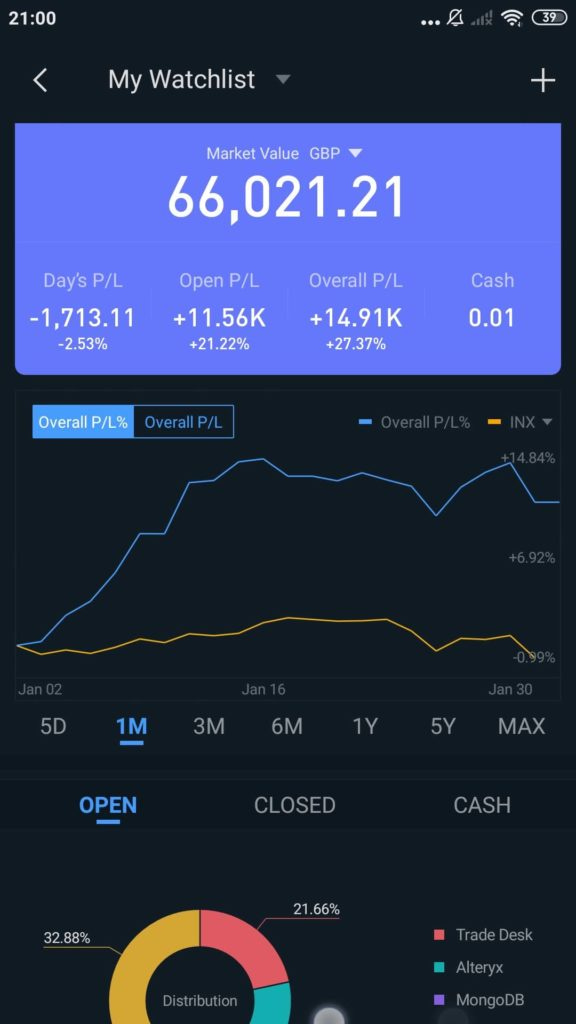

January 2020 Portfolio review

December 31st, 2019 value – £56.6K

Jan 31, 2020 value – £66K

At the end of 2019, my portfolio was significantly down from its July 2019 high, after the meltdown in enterprise software and growth stocks.

January has been an excellent rebound, despite worries in the first week about potential WW3 starting with high US/Iran tensions. My portfolio value has increased by the double digits %-wise, and some names are closing in on their all-time highs.

Portfolio Changes

Added 36 more shares of $LVGO at $26, aiming to build this to a capital allocation of around £7000 over the month. I believe that Livongo is the most underpriced high margin growth stock that I have on my radar, and some excellent writeups have increased my confidence in my decision making with increasing my position. I would have liked to be able to buy more around the technical support level which seems to be around $24 and where the stock price has fallen to at the end of the month, but the post-Christmas pay packet only stretches so far. I do have some $LVGO shares in my Degiro account which I will hopefully be able to add to top out my ISA account before April.

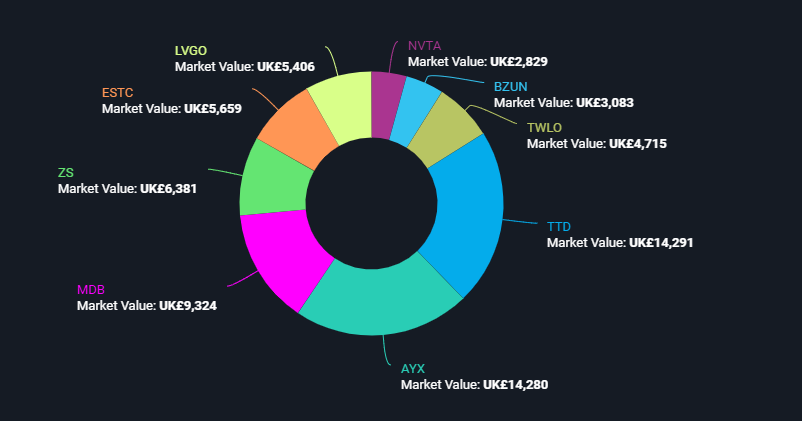

Current ISA Portfolio Allocations in £ (image from Simply wall St)

$TTD

21.7% Position

The Trade Desk had a fairly static month relative to other stocks in the portfolio, gaining 6.5%.

I realise that sounds ridiculous as an isolated statement, but compared to the rebound plays in the portfolio, it is relatively pedestrian. The Trade Desk revenue growth rate dropped into the 30s, clocking around 38%. That is lower than most companies in the portfolio, but they do have the wonderful advantage of being profitable, and they have stellar management in Jeff Green. The long term thesis for The Trade Desk is intact, with the shift of advertising dollars to connected TV and streaming services and they are in a unique position to address the market in China with relationships with Baidu, Alibaba, and Tencent.

$AYX

21.6% Position

Alteryx gained 40% in January alone.

I am a bit disappointed with myself for not adding more when it was in the 90s in December, even noting it on my list of ideas on Jan 1. The truth is that over the Xmas period. I was short on extra funds to allocate to my position, even though it is one of my high conviction ideas – the last ER showed an acceleration in revenue growth to 65%, and an operating margin above 20%.

$MDB

14.1% Position

Gained 27% in January.

Mongo has perked up in January. Its revenue growth is still impressive but seems to be decelerating. The long term thesis seems fully intact, and Atlas (hosted solution) now makes up 40% of revenue. Mongo is also raising more money. With profitability some distance away, I have no issue if they can get it on good terms.

$ZS

9.7%

Gained 20% in January.

ZS went from being priced for perfection to being chopped in half valuation wise and is rebounding slowly. Due to the nature of the product, it requires high-level contact for sales, and the company recognised that sales cycles were likely to lengthen. They remain the best in class product, but analysts are concerned about whether how much the previously blistering revenue growth rates will decline in the short-medium term. I think that long term tailwinds are still intact, and will continue to hold.

$ESTC

8.6% Position

Gained 1.3%

Elastic has gone nowhere in January. Despite posting an extremely impressive set of ER results, the stock sold off early December 2019. It is interesting that Elastic essentially has comparable operating metrics to $MDB, but a much lower valuation. There are questions around ease of use, market dominance, Amazon competition, product strategy, open-source strategy, and profitability. Several thoughtful investors have observed a company like Datadog $DDOG has built APM products using Elastic’s tech, and is outperforming them in business metrics. I would counter that the risk/reward seems enormously in $ESTC’s favour. On the technical side, it looks like a conviction move above $75 would break the downtrend. I am down 25% on my purchase here, but the thesis is intact, so I am doing nothing.

Patience required – the company is growing revenue approx 60% year on year, and I think in time investors will be rewarded.

$LVGO

8.2% Position

Gained 0.3% in January

Partial lockup expiry mid-Jan sent Livongo shares back to where they were at the beginning of the year. Given the triple-digit revenue growth and SaaS like gross margins, cheap 2020 Ev/S valuation, and excellent management. I also feel this is another one where the best thing to do is be patient and continue to add shares while the risk/reward is in my favour. Bert Hochfeld and Richard Chu’s articles on Seeking Alpha have resonated with my feeling here.

$TWLO

7.1% Position

Gained 27% in January

I reduced my TWLO position after 3Q earnings, due to a reduction in the confidence in the management. Specifically, I felt Jeff Lawson’s comments about “revenue growth at scale” were misleading in the representation of Sendgrid revenue and not comparing apples to apples – real revenue growth % was in the 40s and not the 70s. The second issue was a billing error in Q3 and finally a financial error on guidance for the year.

$BZUN

4.7% Position

Lost 9.6% in January

The long term thesis is seemingly intact, but I’ll admit that this stock has not been particularly rewarding to hold compared to the others in the portfolio. Much of this was a result of the trade war, but my confidence in management was reduced after a slow disclosure of the fire at a 3rd party warehouse that the management was aware of but did not disclose during the Q3 call. Poor shareholder governance IMHO.

They have lost Huawei as a customer, and as a result, metrics may deteriorate in the short term. The risk/reward just below $30 seems favourable based on the fundamentals and the long term trend line. There are questions over pricing power and the effectiveness of the transition to the non-distribution business model. Coronavirus may hit ADRs in the short term. Longer-term, this company still has some hallmarks a capital-light compounder, but it would be great to see better transparency.

$NVTA

4.3% Position

Gained 20% in January

Preliminary ER looked like a small miss on revenue, but the long term thesis and 2020 guidance is intact. It’s a lower conviction and higher risk play for me and will remain a smaller allocation than other stocks.

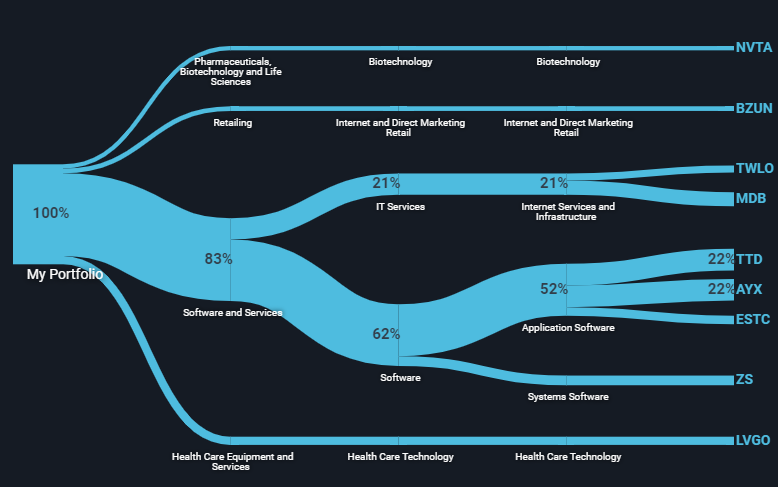

Sector Breakdown (also via Simply Wall St)

Mainly Software.

Overall Portfolio Performance

Despite some dramatic improvements in individual stocks, I remain deeply in the red on some holdings. That is simply a feature of holding these types of companies – you need to be able to tolerate the volatility, or invest in a different style. The long term is the most important view, and the companies I invest in reflect part of my best vision for the future.

Companies on my watchlist: $GSX, $CRWD, $TLRA, $ZM, $ROKU, $YEXT

Loan balance outstanding: £29,802.10

Thanks for reading. I'll aim to post a monthly portfolio summary.