It’s easy to look at return percentages in isolation and feel envious of other people’s success in 2020. Given that many of us on online are friendly strangers to each other, it’s important to remember that you generally have very little idea about the sort of money people are talking about, or what that money represents to them.

There are people managing millions who post on Twitter and elsewhere, and there are people managing a few hundred dollars. Playing comparison and status games is not helpful.

A 200% return on $1,000 is excellent, but the strategy and attitude to risk taken to achieve it might be different from the strategy taken to get the same return on $100,000 or $1,000,000.

Ideally, you would aim for a process that is effective for your knowledge base and personal situation regardless of the amount of money you are managing.

Some impressive investors and traders that I follow who have multiplied their accounts by more than 5 to 10 times in 2020 while managing orders of magnitude more money than me.

Some are more active than I am. Some bought and sold different companies at better price points. Some have successfully used options and margin. I’m happy to celebrate their success but don’t envy them - I’m old enough to recognise that jealousy doesn’t achieve anything. It makes no sense to compare your day 10, 100, or 1,000 of a journey with someone else’s day 8,000. The most important thing for me was whether my investing behaviour and goals matched my intentions in 2020.

Each investor is playing a different game and you must run your own race. You can only do that when you have a clear idea of what you are trying to do. Everyone has their own investing philosophy - what’s yours?

I’m grateful for my unusual 2020 returns, but my portfolio pales in comparison to the overall picture of outstanding debt and my long term goals.

Given my situation, would it be useful to compare myself with someone who has paid off their mortgage, earns 5 times more than I do, and is managing a multimillion-dollar portfolio?

I don’t think so.

I can certainly learn from them, but because their situation is so different from mine, there is a limit to how much value direct comparison would yield. You don’t know anyone else’s financial position in the detail you know your own. It’s not a valid comparison.

In addition to different goals, everyone has a different range of ongoing commitments and debts: business costs, childcare, education, mortgages, healthcare, and support for older family members.

If I was 2 years from retirement, it’s entirely probable that my portfolio strategy would differ from what it is today.

On top of that, investing conversations are global, but there is also a huge variation in taxation around the world.

Focusing solely on posted returns ignores all these factors.

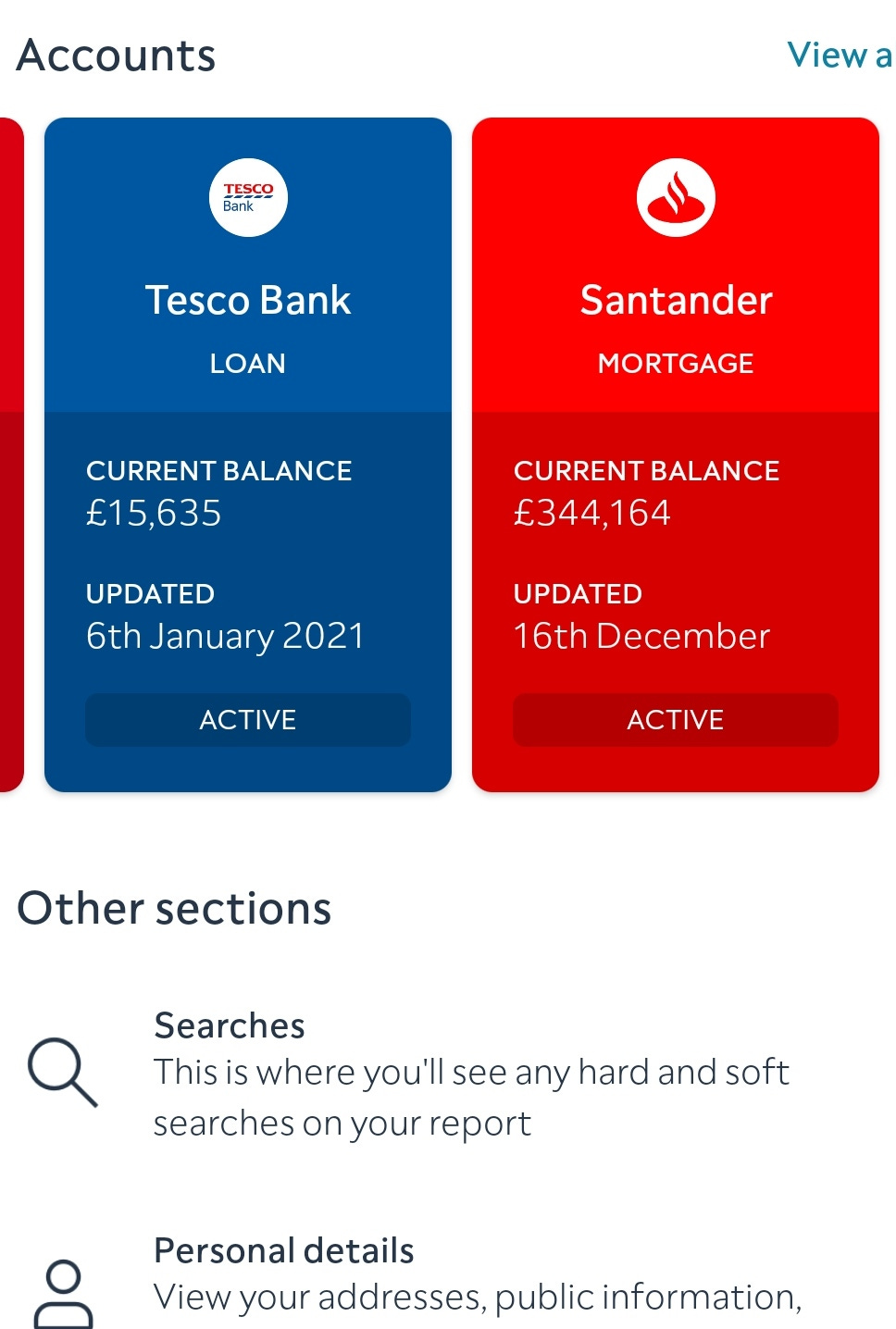

I still owe about £15.6K on my investing loan. The minimum payment on the loan will be about £4,000 in 2021 - that would leave £11,000 to clear the balance. If I put the monthly ~£150 freed up from clearing the car loan in December, then I could realistically pay off £6,000 in 2021.

We have 3 kids, and I put a lot of thought into trying to maximise their future options. The best way for me to do that is to focus on a sustainable growth trajectory for my investments. Someone with no children, no desire for them, a low cost of living and looking to lean FIRE might optimise differently. We are all wired differently and are operating on different time horizons.

I still have a lot of work to do. I’m fortunate to have access to job security and a defined benefit pension. NHS salaries won’t make you wealthy (band 8C range since you asked), but the jobs are pretty secure and the pensions are decent. The bulk of my NHS Pension will be from a career average scheme. Knowing that I have this makes it much easier for me to take a more aggressive approach to my investments. Someone in a different situation, with a less stable job situation, might take a completely different approach to their personal finance. It’s personal for a reason.

I was recently accused of being a charlatan because I wouldn’t tell a stranger on the internet what stocks they should buy.

Ignore the lack of basic politeness for a second. Ignore the fact that I’m not a registered financial advisor. I really don’t think that any reasonable person should expect an answer to this question from a random person on the internet.

I won’t ever tell anyone what stocks they should buy, so please don’t expect me to. I don’t know. It will depend so much on what you are trying to achieve and many other factors. I can only make decisions for myself and will own the consequences in either direction.

You have the best insight into your financial situation and goals, so make decisions that make sense for you. Own it for the long run.

Your future self will thank you.

P. S. For another perspective on why comparison is pointless, check out this great article by StockNovice