April 2020 Portfolio Review

From the misery of March to an awesome April...the stock market is not the economy

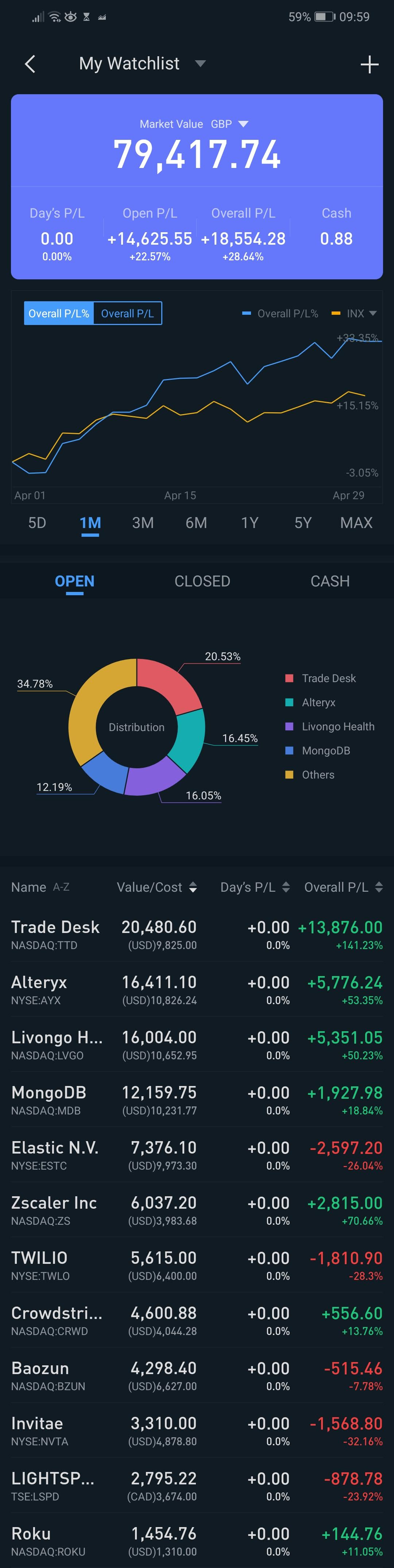

Portfolio Value

Feb 29, 2020 value - £75.3K

Mar 31, 2020 value - £62.7K

Apr 30, 2020 value - £79.4K (up 26% from last month)

YTD ~ 29%

No financial contributions to the portfolio this month.

Portfolio Graph

Overview

Well, morale has improved after March’s beatings. I’ve gotten a lot of value out of connecting with experienced and thoughtful investors on Twitter - if that is you, thank you!

My portfolio is at the highest month-end for 2020 so far, but my P&L% is still down from mid-February peak. This is because I added cash to my portfolio at the end of February. Livongo has been my April portfolio MVP.

It has been a rather bipolar couple of months.

Portfolio Changes since end-March

None.

I wrote about planning to deploy further capital in April - May. The strength of the rebound has surprised me a bit. Given the strength of the portfolio performance and the level of uncertainty around ERs and forward guidance, I am holding off for now.

I don’t spend a lot of time obsessing over macroeconomic issues because they are outside of my control, but there is a huge level of global uncertainty right now due to the current global pandemic and many unanswered questions about timing and strategy of the restart of global economies.

At the same time, organisations are starting to quickly adjust to the need for digital transformation, a key investment theme of mine.

The tailwinds are definitely there.

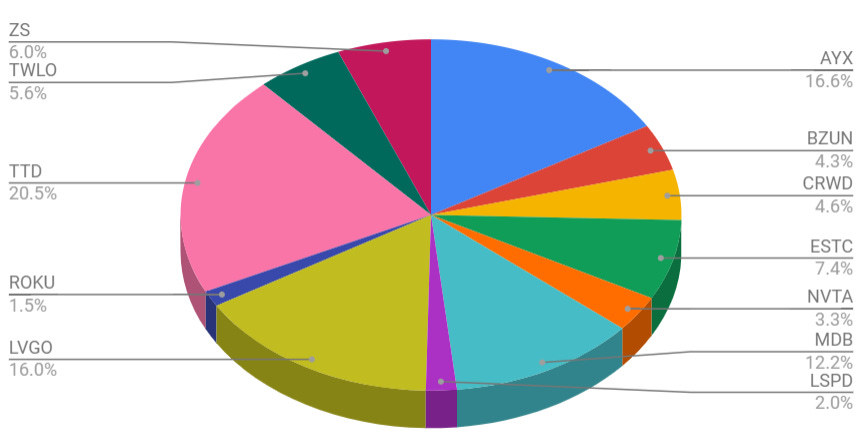

Current Portfolio Allocation

Last 30 Days Individual Stock Performance Summary

$TTD

The Trade Desk is up about 47% this month after losing over 50% at the lowest point in Mid March.

I was desperate to add another 10 shares around $150, but decided to hold off due to having a sizeable position in $TTD already, staying within my portfolio management rules, and building a bigger cash buffer for our personal finances.

Jeff Green has posted an optimistic video outlining one of the effects of Covid-19 in accelerating the shift to connected TV.

The company may still see a short term hit in revenue growth, but the long term trends are positive. I have decided not to try to game the movements on the Trade Desk unless the thesis changes.

$AYX

Alteryx is up 21% this month.

The market seems a bit unsure about the short term effects of stay at home on the business prospects for $AYX. The product doesn’t play into the work from home theme as it seems to be largely used on-premise, and it seems there is caution regarding the impact of COVID-19 on sales guidance.

Regardless of the short term impact, the long term thesis for Alteryx is firmly intact, and I continue to hold.

$LVGO

Livongo has been undervalued since I first came across it.

I wrote in my Feb review that $LVGO was “exceptionally undervalued for the revenue growth it has shown to date. Livongo is a leader in a new market and may take some time to demonstrate its leadership to Wall Street.”

Well it seems that institutional investors are starting to agree with me. $LVGO is up over 40% this month after the Founder was featured on CNBC and they preannounced first quarter results and extended their range of partnerships. They seem to be benefiting from Covid-19 driven healthcare transformation.

No concerns here.

$MDB

Up 23% in the last month.

Solid relative strength. Named the Google Cloud Technology Partner of the year for 2019. Some investors have expressed reasonable concerns about revenue deceleration and limited improvement in operating margins, but I may have a slightly longer time horizon than many, and no alternative that compels me to act.

$ESTC

Up 19% in the last month.

Elastic has underperformed for me to date, but I honestly think that is a reflection of me overpaying on valuation and not sticking to my rules on scaling in, rather than anything being wrong with the company.

There is some skepticism over Elastic’s business model and questions over a perceived lack of focus, but they are executing will and in time, the stock price will reflect this. They are still growing revenue >50% at an impressive scale, so I continue to hold as nothing has changed my thesis so far.

$ZS

Up 14% this month.

WFH tailwinds have reignited interested in Zscaler and they recently posted insightful videos on enabling a big Australian bank and the FCC. $ZS is expensive relative to most recent ER performance, so another short term beating would not surprise me.

$TWLO

Up 16% in April.

Competitor $BAND posted solid results this week which should bode well for $TWLO’s upcoming ER.

Jeff Lawson posted an insightful series of Tweets that give me confidence in the future of the company and they issued a PR on Telehealth integration for the backend of a system by Epic.

$CRWD

Up 15% in April.

It took a little time after the ER, but Crowdstrike is rebounding nicely and the executive team are confident that endpoint security demand will be increase with increased WFH.

$CRWD have a partnership with ZScaler and the tailwinds should benefit them both.

$BZUN

Up 18% this month.

When I first bought shares of Baozun in 2017, it was the category leader in the important emerging market of China brand e-commerce. That remains true, and though it has been a frustrating stock to hold, the thesis is still intact so far. Many Chinese ADR have had a number of potential risks, but for now, it remains part of the portfolio though I have no intention to add to it. Some encouraging words were released by the Chairman this week, and they recently filed their 20-F which I intend to review over the next week.

$NVTA

Up 17.5% in April.

A rebound that doesn’t seem to have an obvious catalyst other than reversion off the low - I would not be surprised by more pain around ER.

$LSPD.CA

Up 34% in April.

I hold a small position in Lightspeed POS, but their SMB and restaurant base has been heavily impacted by the shutdown. It is likely to face continued short term headwinds. Pondering.

$ROKU

Up 39% in April. One of the most volatile stocks I have watched over the last 18 months. The long term CTV thesis is intact. Still a small position for now.

Decision Making and Mastering Your Process

I strongly believe that optimising your thought process will improve your outcomes. I’ve spent a lot of time in April reflecting on my own decision-making and historical errors of judgment. I’ve come up with a decision making framework for identifying, selling, and risk management of high growth stocks that will serve me well in the future, and got some useful feedback after sharing them on Twitter:

I identified the traits of an ideal business here:

and these traits explain why the bulk of my portfolio consists of Software as a Service (SAAS) companies.

Position Sizing in a Concentrated Portfolio

Articles and Podcasts Worth Your Time

Bessemer State of the Cloud 2020

Meritech Capital Enterprise Software Comparables

Meritech Capital Consumer and Healthcare Comparables

Podcast on Cloud Giants and Growing a Business In an Economic Downturn with CEOs of Shopify, Twilio, and Pinterest (reflecting on 2008-9)

The Loan

Loan balance outstanding: £28K

Loan to portfolio value (LTV) rate: 35%, down from 45% last month

Summary

April has been a wild ride and I do not know whether we will retest the lows and neither do you.

Digital transformation and work from home companies have rebounded strongly for now, but it seems too early to get visibility into what Q2 or Q3 will bring.

I expect earnings season to be volatile, so I am better off focusing my energy on making sure I am happy with my portfolio and holding great companies - it’s one of the few factors that is really under my control.

Stay safe.

Watchlist

$SE, $SMAR, $WORK, $EVBG, $TXG

ER dates to watch:

May 5 AMC: NVTA

May 6 AMC: AYX, LVGO, TWLO

May 7 AMC: ROKU, TTD