December Q4 and 2021 Year in Review

I paid off my loan, underperformed the indices, and learned a lot

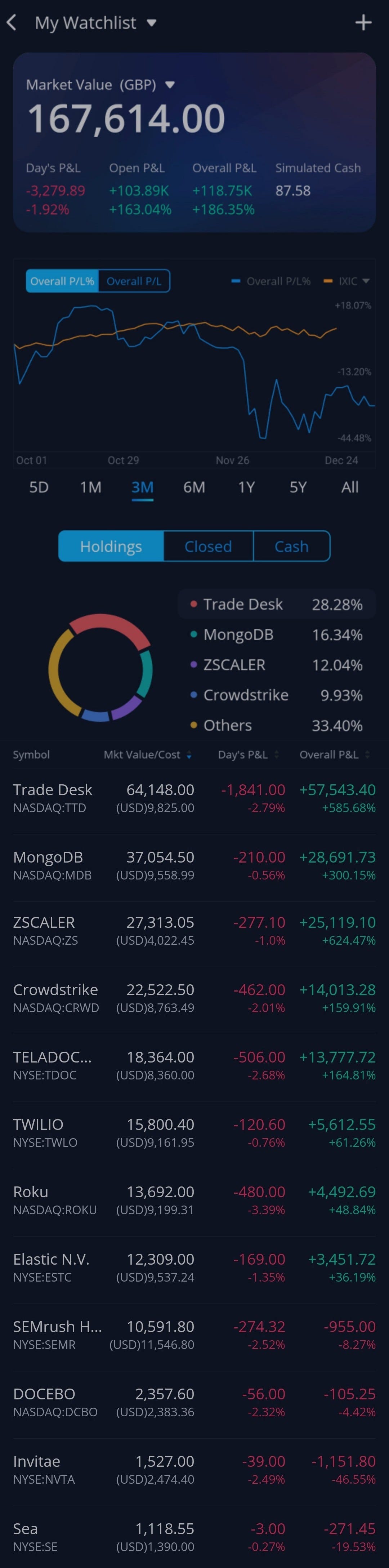

Portfolio Value and Links to Previous Quarterly Reviews

YTD -7.5 % (including withdrawals, excluding crypto)

YTD 1.2% excluding withdrawals, excluding crypto

YTD 8% excluding withdrawals, including crypto

End Q3 2021 value £165K – loan owed: £0

End Q2 2021 value £181.6K - loan owed: £4K

End Q1 2021 value £157.1K - loan owed: £9.6K

End Q4 2020 value £181.6K - loan owed: £15.6K

End Q3 2020 value £153.1K - loan owed: £16.6K

End Q2 2020 value £124.7K - loan owed: £27K

End Q1 2020 value £62.7K - loan owed: £28.6K

Dec 31, 2019 value £56.6K - loan owed: £30K

Q4 2021 Overview

My stocks are generally flat on the year.

My portfolio value is lower as a result of paying off the loan. Most of the gains that I have had in 2021 have come from crypto. That is adequate, but I feel I could have done better. It has been a continuous learning experience for my stock journey. Getting the balance right on risk management is one of the hardest things.

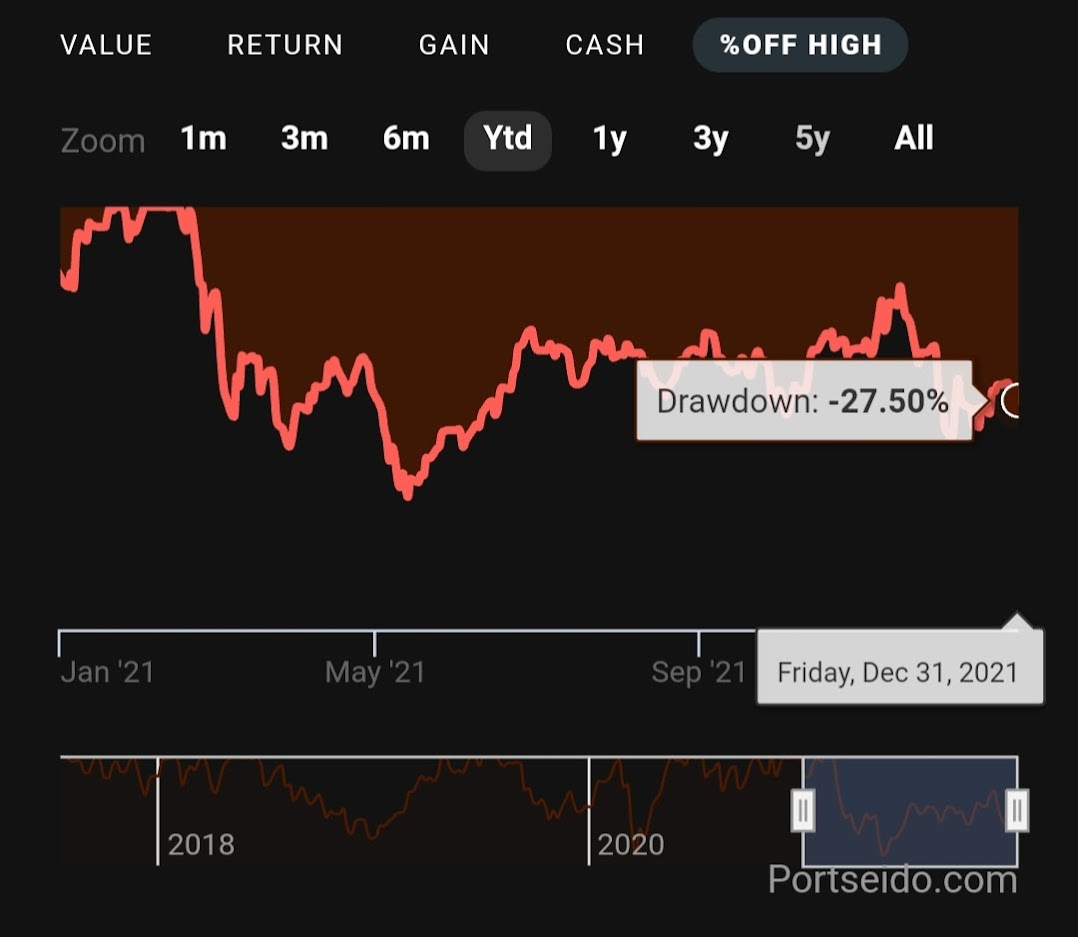

February 2021 was a crazy time, and I recognised that looking at the timing of this tweet…

I didn’t fully take advantage of the euphoria.

Stepping back a bit, I'm content with where I am over the longer term. At the end of 2019, my net position was ~ £26,600 and my current position is 6x that 2 years later. That is the power of ̶l̶e̶v̶e̶r̶a̶g̶e̶ perspective, and I’m grateful for where I am despite the setbacks.

Portfolio Changes since the end Nov 2021

Sells

$CLPT

This was a small tryout position for me, and the ugly general pullback has focused my attention on my core holdings. I’ve sold it as I don’t understand it well enough, but it will stay on my watchlist while I try to learn more.

Buys

Topped up $ESTC a little and added a small amount more $SEMR

Despite appearing like the second time after May that it would be good to deploy cash, the majority of my intended December spending was already tied up with Christmas plans…

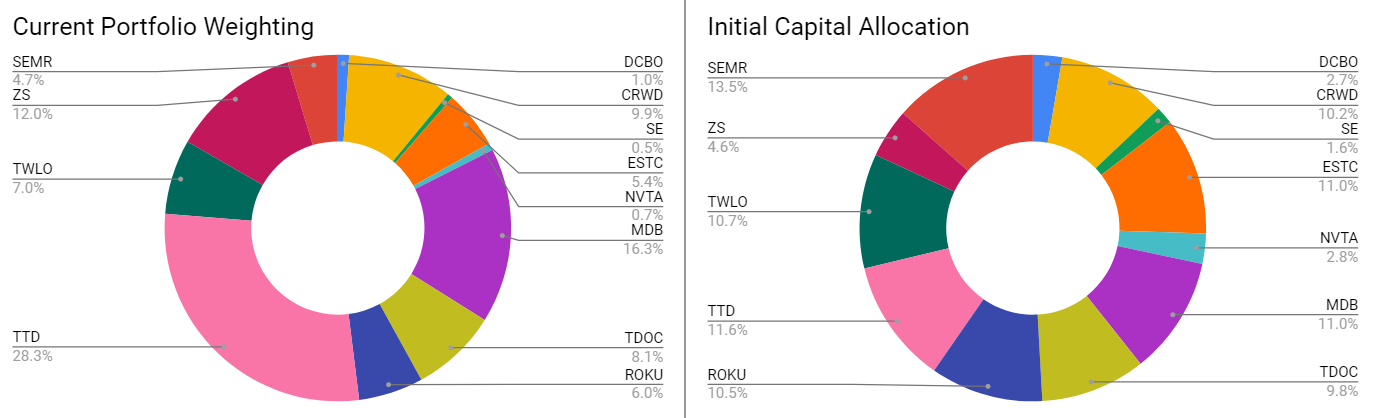

Current Portfolio Allocations

Company Earnings

Results are clickable from Tickers below

TTD

ER was solid. Fast, profitable growth in an industry with secular tailwinds but without the compromises of media ownership and walled gardens. The company recently announced more international support for UID 2.0 and ad-buying on Peacock.

I don’t have execution concerns with $TTD but valuation remains a risk in the near term.

MDB

ZS

ZS has a strong 2021, and execution wise, I’m impressed. It is a shame that I didn’t back my appreciation of their execution with more capital during the year, but it has been hard to find an attractive point all year. The position size has grown impressively despite my under allocation, but as a result, valuation remains a risk. It’s a similar position to how I see NET - great company, great CEO, but at a significant market cap, it is hard to find an obvious place to add outside of the 200DSMA.

CRWD

CRWD continues to execute well, but a number of eyes have drifted towards SentinelOne and the story of “better numbers”. To me, it’s a complex picture. Both companies are doing well. It’ll be interesting to see how it plays out, and the market cap differential is important.

TDOC

I felt Investor Day was mainly a reiteration of what we previously knew. Most holders of TDOC have had an ugly drawdown amidst negative sentiment. I may have erred in holding on all year. It’s a good example to remember that investing in what is, rather than what could be is often simpler and more efficient. This video touches on the current criticisms and negative sentiment on TDOC.

TWLO

Ugly price action, but the company is looking to support the building of an ecosystem around its product suite via Twilio ventures. The guided future growth is attractive, and I still rate Jeff Lawson - Ask Your Developer is on my reading list for 2022.

ROKU

Still growing, but competition by well funded capable companies is building a wall of worry…

ESTC

I thought the quarter was fine. The consistent low balling of growth by the CFO is taking its toll. Elastic cloud is growing well, but the company looks like it’s destined to be the ugly sister of MDB from the street’s POV.

SEMR

ER showed 50%+ growth, but my take after listening to the Q3 call was that it’s tougher to sell investors on the opportunity when you are communicating in your non-native language.

Priced their public offering at $20.50, and seem to be executing well as a business.

DCBO

I’m still learning about Docebo. Topline growth seems solid and it’s good to learn more about the history and founder. I liked this 2- year old video from their post IPO days that gives a little historical context. I don't know how big the business could really get.

NVTA

There is little new to say here. It’s a lower conviction speculative position that I probably should have sold higher because my questions about sustainability are hard to answer on the current trajectory. Considering selling it to add elsewhere.

SE

I nibbled a little on Sea Limited at the 200DMA. It’s pulled back another ~20% from there but seems to be basing around $200. In an alternative universe where I had more capital, I would have been slowly adding around that level with a 3-5 year horizon. In the near time, it’s harder to be confident - bad things generally happen below the 200D SMA.

10 Things I re-learned about investing in 2020

These are mainly things that I already knew, but sometimes you have to be hurt to be reminded.

A clean narrative and outperformance vs forward expectations are key fundamental drivers of returns. Companies that struggle with the clean narrative test include $ESTC and $TDOC. The narrative has been getting more complex with $ROKU, $API, and $LSPD.

It’s probably a good idea to sell lower conviction holdings if/when they have appreciated significantly in value. This would have helped with movements in $NVTA, $API and to a lesser degree $TDOC in 2021. If a lower conviction company that I hold 3x’s in value over a 6 month period from now on I will be more likely to trim it than not.

There may only be 2 great opportunities to buy per year. For my companies and their peers, early May and mid-December looked decent. This is always easier to identify in retrospect.

Building a strategic cash position when valuations are unfavourable allows you to take advantage of 2. I wonder if I should try to restrict all purchases to a maximum of 3-4 times a year.

Fintwit encourages short termism, schadenfreude, and instant gratification. If maintaining a long term mindset is important to you, be mindful of how much time you spend there.

Having a consistent system that you can stick to is probably more important than optimising for absolute returns.

Having a sizeable debt burden will likely harm your ability to make clear-headed financial decisions. This is the main reason I don’t buy on margin and why I’m glad to be rid of the loan.

If a company is not operationally out-executing the high bar you set for it to remain in your portfolio, it needs to be kept on a very short leash. Decisive selling is something I need to consider more closely.

Entry price matters a lot. A great company at the wrong price, and in the wrong size allocation can hurt you in the near term.

Companies that demonstrate high relative strength in a selloff should be high priority considerations for portfolio addition. The corollary is that the generals get shot last, so you have to be careful about timing.

What’s next for 2022?

2022 is likely to be a year of transition for me. I am in the process of applying for an overseas role. It’s still in the works but would likely mean that if we were to take it up, it’s likely to have an impact on how I think about our family finances and investments. It’s likely that I may need to use some of our investments as capital for the transition.

In the long term, I think it will be a worthwhile move for us in terms of life experience and adventure, but I can’t sell it as a “sensible” short term financial decision. The setup costs are significant, and we’d probably be going from a dual income to a single one, and a higher cost of living from where we currently live.

This begs the question, why do it?

My career is at a stage where I have the chance to have one final adventure before being so settled that it is less likely that we would take the opportunity for randomness

Everything feels a little too predictable on our current trajectory - it’s all “fine”, and secure, but there isn’t much to be truly excited about

I want our kids to grow up understanding that you can change your life by making decisions that in the short term don’t look “sensible” but add to the richness of life

The weather, work-life balance, and lifestyle is better

The organisation has a great reputation that is likely to open doors down the line for me when we return

I have always believed that financial decisions need to be considered in context. I write to document my experiences and to make myself accountable. We all have different goals, so I appreciate that my decisions may not make sense to you - that is OK.

All the best for 2022!

Watchlist

$DDOG, $NET, $MNDY, $SNOW, $MELI, $AMPL

Great to hear from you again at length. Wishing you and your family best of wishes with the potential career change.

P.S this part "That is the power of ̶l̶e̶v̶e̶r̶a̶g̶e̶ perspective, and I’m grateful for where I am despite the setbacks." made me LOL.

Thanks for putting it out there and sharing your story.

Conor

Hi ADIFI, well done for remaining accountable in this journey. I wanted to ask you about your lessons learned. They all seem valid, but also very micro-focused.

Given the macro sledgehammer being taken to the market at present, are there not lessons there also i.e. like just as you couldn't really lose in late 2020, you'd struggle to pick any spec-tech winners in January 2022 regardless of all the tips and tricks in the book?

Secondly, any considerations re: the whole active/passive debate at large? Assuming you still feel you have an edge (?), is this horrendous volatility suitable for your goals?