June and Q2 2021 Portfolio Review

Back again, and why I don't mind too much that my stock portfolio is flat YTD.

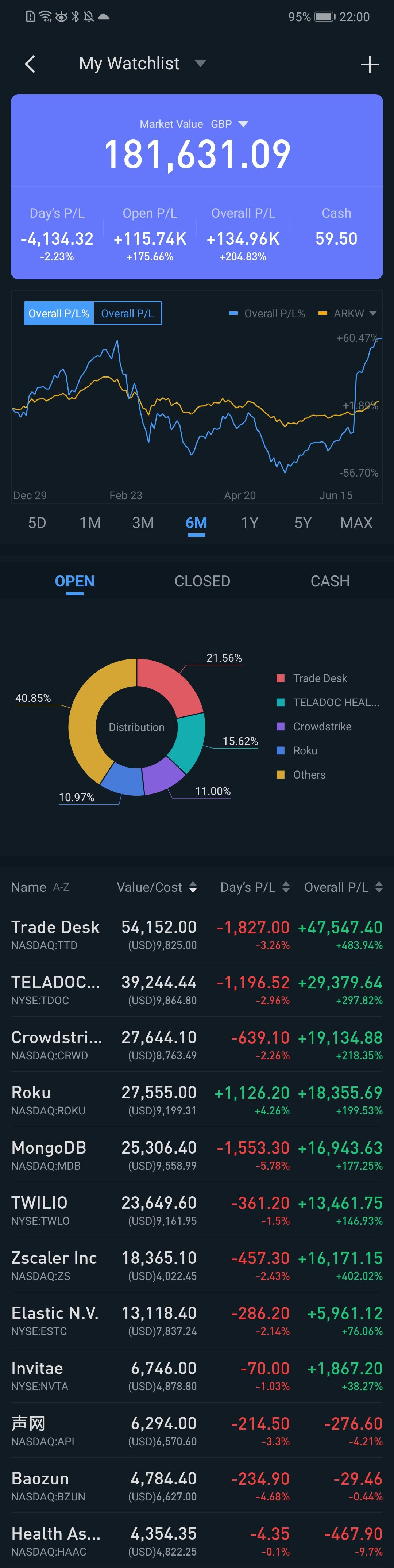

Portfolio Value and Links to Previous Quarterly Reviews

YTD -3.3% (includes withdrawals)

Q2 2021 Overview

Ladies and gentlemen

Front, left, right

Back again

On pullbacks:

Never too late to prepare…

”Cause many things you fear have been in place for years.

My portfolio bounced and I caught a rebound.

Q2 had its challenges. I was mentally prepared for a -35% pullback, but it ended up as a -40% pullback. May 12th looks like it was the bottom for my portfolio - so far…(image via Portseido).

Given the pace of the bounceback, another near term pullback wouldn’t surprise, but I have no idea.

It's funny how the last 5% drop often feels like the most painful even though the monetary value of the loss is significantly less than the earlier part of the drop.

The hardest part for me during this time wasn’t so much the experience of the drawdown - I’ve gotten relatively used to those. It was my inability to deploy further capital during a time when the risk/reward was finally favourable because I had committed to paying the loan off early.

I think that there are probably only two or three times a year that the risk/reward is really in my favour for the majority of stocks that I own or like.

My mid May virtual shopping list included…

$SHOP at $1050

$GHVI below $11

$ESTC at $101

$TMDX at $22

You get the idea. All of those were solid ideas on companies I have researched and believe have the potential to be high-quality growers, and could provide an attractive return at the prices above.

Although I still don't believe I can time the market per se, it's not hard to appreciate that future returns start to look more attractive with a portfolio like mine after a -35 to -40% pullback, when Fintwit sentiment skews negative and the victory laps of sideline rubberneckers are on display.

For reasons I explained last month, I am persevering with the plan to clear the loan before Christmas 2021.

Loan clearance is within reach, and I'm going to do it. There will be other opportunities to invest in the future. I just need to be patient.

Watchlist Overview

Portfolio Changes since end May 2021

Sells

None

Buys

10 $API at $38.79

Current Portfolio Allocations

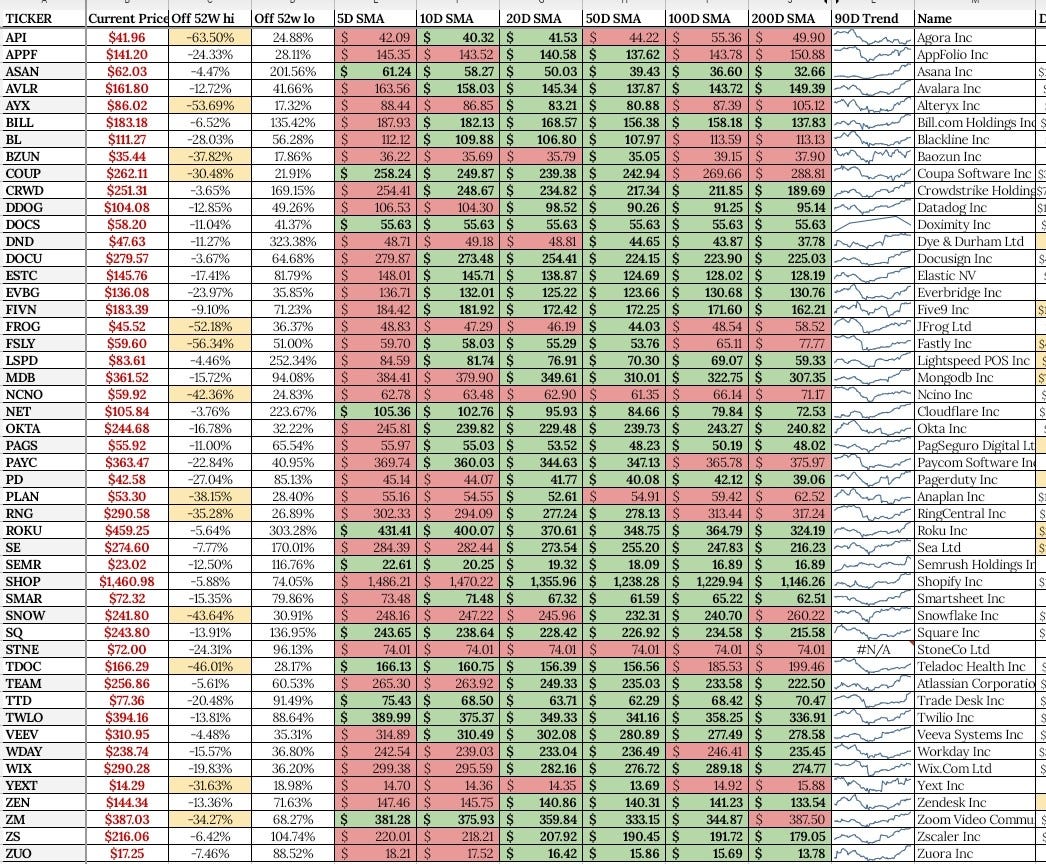

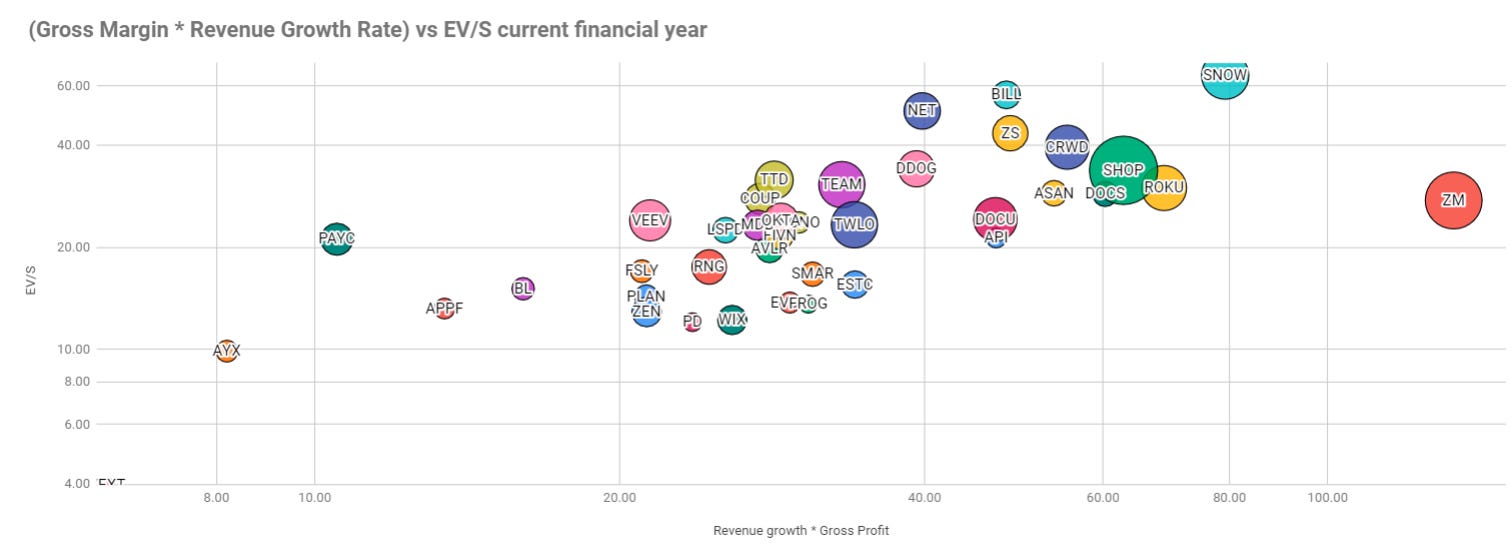

Company Reviews - ER results are clickable from Tickers

TTD

A decent recovery from May and a 10:1 stock split. A big bump on the deferral on Google’s 3P cookie deprecation till 2023.

I largely agree with Kris FGTV on this one. It’s volatile and expensive, but I think it can still provide attractive returns over the long term.

TDOC

Still out of favour and readily dismissed on Fintwit as a COVID19 beneficiary commodity with no technology moat. Success in healthcare technology requires scale distribution, integration and successful relationships in addition to good technology.

There are some interesting questions about the future of telehealth demand, the acquisitive nature of $TDOC’s growth and the premium of the $LVGO takeout, so digestion is still going on.

Let’s see if stock price improvement changes sentiment over the next year.

All that said, I’m very open to slicing some of this to invest in $DOCS nearer lockup expiry in December…. Somewhere under $6B would start to get me interested.

CRWD

Little to worry about at the moment bar the potential issues around valuation, but I was amused at this shade by $S

MDB

Atlas remains the company MVP as they continue to surf the wave of developer led growth.

It’s not just developers at forward-looking companies. Mongo’s flexibility is attracting the attention of the government in the US and around the world.

I’d like to see a little more interest in profitability…

ROKU

Another excellent quarter for ROKU - my key questions are on how well they will do outside of the US vs incumbents like Samsung and LG, whether they evolve to integrate into smart homes, and whether AVOD becomes as big as everyone expects. There isn’t much to complain about on the ER metrics.

TWLO

Strong gross profit growth, a couple of acquisitions, good customer growth. and a consistently high net expansion rate.

- Discogs")

Operational leverage would be nice to see at their size, but I am ok leaving it to Jeff L for now.

Irnest has a nice summary.

ZS

A great ER, and one of my more rewarding investments to date on a % basis - just not in absolute returns. A pity I’ve historically undersized the position - initially due to valuation, then due to execution issues which are since resolved. I’m now a bit cautious for valuation reasons again, but I might consider rebalancing a little of my $TDOC here if/when it recovers. It seems a little odd that I’ve allocated more capital to $API than I have here, even though the position sizes are different as a result of the performance.

ESTC

The spectre of Amazon continues to loom over Elastic, but over time, I think the aggregation of marginal gains will play out in Shay and co’s favour as long as they continue to execute and deliver strong ROI for their clients.

If you haven’t yet, take a moment to read this excellent overview of Elastic by the guys at Deliberate Capital.

Glancing at Elastic’s balance sheet, I’ve wondered more than a few times in the last year whether they would take advantage of cheap money - turns out that the answer is yes.

NVTA

Earnings were more of the same. Price action ugly of late. Genetics is outside of my core area of expertise. The position has been sized appropriately as a result. If it works out in the long term, it’ll be worth it. But it might not. ¯\_(ツ)_/¯

API

No market love for Agora and a textbook demonstration of why entry price matters. If I had bought a full-sized position on Clubhouse hype and because the chart in Jan-Feb was going up and to the right, this would be a much harder hold. $10B was clearly not justifiable in February.

As it stands, I think that social audio is a real tailwind and whether Clubhouse, Greenroom, Facebook audio, or something else, there will be an increased demand for something like Agora’s services over the next decade. I made a small addition this month.

The decline on the back of the regulation against Chinese EdTech is understandable, but there is value in looking past the price action. Let’s see how it plays out over the longer term - they might have what it takes to become a platform.

BZUN

Sometimes you are early. Sometimes you are wrong. I think it’s probably the former, but it’s felt more like the latter with me and Baozun - flat for 4 years. Do I hold on? I can take the pain, and am pretty headstrong, but am looking dead wrong here so far.

In the meantime, the company has kept executing reasonably well, earnings are growing faster than revenues and the thesis seems intact, but this has been dead money to date.

This update from FullJet on LinkedIn suggests that they are building momentum going forwards, and the pace of acquisitions and strategic alliances is on the up.

HAAC

I'm still not yet completely immune to FOMO. I bought $HAAC too early due to SPAC over-enthusiasm early this year. The downside is capped, but truth is that capital here would have been better deployed into one of the real companies mentioned above at an opportune buy point. Part of the reason I drifted into this position was due to concerns with valuation in my usual pockets of the market. When the environment changed, I should have been swifter to act.

Some of this position is likely to be sacrificed towards loan payoff in Q3, regardless of DA status.

What I’ve been listening to this month

Ho Nam on the Acquired Podcast

Ho Nam has quickly because one of my favourite people to learn from on Fintwit.

Yen Liow Speaking at Oxford University

A great perspective of what it takes to succeed at investing over the long term, balancing the art and science, and some process insights.

The Loan and my investment “balance sheet”

Loan balance outstanding: ~ £4K

Loan to portfolio value (LTV) rate: 2.2%, down from 6.1% end Q1 2021.

The usual thing to do is to look at my portfolio purely in terms of the market value of the stocks. However, I’ve always been acutely aware of the overall position net of the loan outstanding - a variation on the idea accessible net worth if it were a balance sheet. Home value is largely irrelevant for these considerations from my perspective - although our house is also technically a levered appreciating asset, we will always need somewhere to live. Any value there is not readily accessible unless we moved to somewhere with a lower cost of living - less likely in the near term imho.

The graph above is a much closer tracker of my perspective over the last 18 months, taking not only my portfolio value but also the outstanding loan balance into account. It’s not a graph of returns but helps explain what drives some of my decisions regarding asset allocation and loan payoff.

The reason it has been easier for me to “not care” much that my stock portfolio value hasn’t appreciated YTD or that I’ve had such a steep drawdown is my appreciation of how transformative the last 18 months has been for our family’s finances. My approach certainly got off to a rocky start…

Using leverage has its risks, especially if you aren’t prepared for the worst-case scenarios.

My experiment has worked out well, whether through luck, judgement, or that awkward grey zone. Discipline is critical in your approach to personal finances, investing, or in fact almost anything of importance.

I’m approaching 4 years of investing experience in Q3 but still have a lot to learn. I spent the first two years of investing (2017-2019) making rookie errors - choosing good companies but not having the right buying process, holding discipline, or a clear philosophy, and being far too susceptible to FOMO and MOMO chasing.

Learn from your failures. I became much more intentional about my investing strategy in Q3-Q4 2019 when I started this blog. I started to feel that I had found a rhythm and process I could work with. It was fortunate timing.

Back in Jan 2020, I was fully committed to the prospect of paying off the loan over the long term. The loan was affordable, my job has stayed secure, and I believe I had successfully kept the risk of ruin within my acceptable limits by not using margin or options.

2020 was obviously an outlier. C19 has been awful in so many ways, but my portfolio ended up hugely benefiting from the accelerated digital tailwinds that followed. Some people have been lucky enough to increase their savings rate during lockdown. As a result, I’m lucky enough to be in a position where I can get rid of the loan earlier than I ever dreamed of. But I’ve still got much to learn and am still refining the way that I invest.

You could make the argument that paying off the loan early might reduce overall returns.

It is probably true. But if I can’t obviously see the asymmetry, I don’t want to live my life that way.

The trade-off: yes, I am likely to miss out on some opportunities while I do this, but I really am OK with that when things are put into perspective. I’ve watched a number of watchlist companies strongly rally in the last couple of weeks, but I no longer get much FOMO when I have so much gratitude. I’m nowhere near financial independence, yet feel like I’ve had some significant steps in the right direction over the last 18 months. It definitely has been an adventure - at least I picked an appropriate pseudonym!

Twitter Spaces

I had a blast participating in my first Twitter Spaces skillfully hosted by IQ and Buyandhold. We got to learn from Alex at TSOH and StockNovice.

The topic was Starting with the Basics.

Have a listen to the recording and let us know what you think!

Outside of work and investing, I had a fun Father’s day.

The medal is the judgment of a toddler, but I’ll take the win. We’ve delayed and rebooked a trip to the Balearics but all the fluctuations around international C19 rules and the cost of testing everyone mean I have no idea whether we’ll actually manage to leave UK shores this summer.

Might have to go camping instead (ugh).

Have a good July!

Watchlist

$DOCS, $SEMR, $CLPT, $CMLF

Hey, great write up, it sure has been a challenging year. I see TTD is your largest position, I have been reducing mine to account for the potential cookie risks. It looks ok at the moment due to the delay, but still will unified 2.0 work? I still like this company a lot. But need to allocate appropriately. Your last point about FI is interesting and something I have been thinking about. How much do you need? If you can earn 20% per annum returns then you only need 180k in an ISA, 360k @ 10% and 720k @ 5%. All depends on the risk you want to take to earn your FI 😎