October 2020 Portfolio Review

Halloween fright to finish the month.

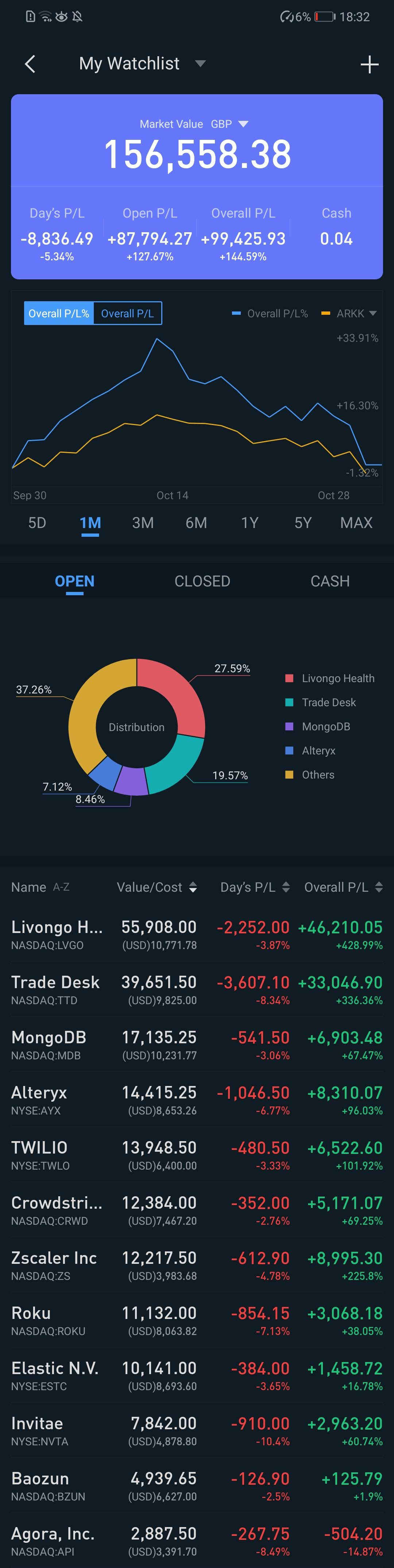

Portfolio Value and Links to Previous Monthly Reviews

August 31, 2020 value - £145.4K

October 30, 2020 value - £156.6K

YTD ~ 138% (from +133% last month)

Financial contributions to the portfolio this month: ~ £480

Overview

The original version of this post got lost in the Substack ether, so I’m publishing this incomplete one now and will add back to it slowly.

If September was the introduction to volatility, October continued along the same theme. The month ended with a whimper, after peaking with a boom in the middle. My portfolio peaked at £180,000 on Oct 13th and prompted my personal trigger that things were getting frothy: I talked to my wife about the stock market.

I am self-aware enough to recognise this remarkably consistent indicator of a short term top, I’m not yet skilled enough to fully capitalise on the recognition.

If I was, I would have sold the peak, paid off the loan, bought back in, and still been up for the month. But I am not an expert in market timing - so it goes. I try to optimise for what I can control.

There are a lot of reasons for volatility right now - thoughts on the US election, a regular pullback in technology companies that has diverged away from moving averages for a while, easing into earnings seasons, further lockdowns in Europe including the UK. For now, I’m satisfied with buying and holding, and simply accepting volatility as the price of admission. I simply don’t have enough of an edge to try to get clever.

The volatility started to look like it might start to recede towards the end of the October…

but it turns out it was just a headfake…

The biggest victim of the volatility was former Fintwit favourite $FSLY (no position) which went from Usain Bolt at the 2008 Olympic Games 100m final….

To Usain Bolt at the 2017 World Championships 4x100m final.

Portfolio Changes since end September 2020

New contributions: £480

Sells

$AYX

Sold 25 shares at ~ $144.5

Buys

$CRWD

Added 10 shares at ~$148

$ROKU

Added 10 shares at ~ $207

$API

Added another 15 shares of API at ~ $41

Current Portfolio Allocations via Google Sheets

Company Reviews

$LVGO

This will be my last month as a Livongo shareholder, and the stock has ended flat for the month.

Livongo released another outstanding ER, beating the projected estimates that had not been formally given out at the prior ER.

Livongo Q3 Fiscal 2020 Financial Highlights:

Revenue: Total revenue for the quarter was $106.1 million, up 126% year-over-year, driven by the continued adoption of our Applied Health Signals platform.

Gross Margin: GAAP gross margin of 75.6% and non-GAAP gross margin of 76.3%.

Net Loss and Non-GAAP Net Income: GAAP net loss of $25.5 million, and GAAP net loss per share attributable to common stockholders of ($0.26) on a diluted basis; and non-GAAP net income of $19.2 million, and non-GAAP net income per share attributable to common stockholders of $0.16 on a diluted basis.

Adjusted EBITDA: $20.7 million in the third quarter of 2020.

Livongo for Diabetes Members: Over 442,000 as of September 30, 2020, up 113% year-over-year.

Livongo Clients: 1,402 Clients as of September 30, 2020, up 71% year-over-year.

Estimated Value of Agreements (EVA): $145.9 million up from $85.5 million in the third quarter of 2019, representing 71% growth year-over-year. EVA consists of the estimated value of agreements signed in the quarter with new Clients or expansions entered into with existing Clients.

The merger received 99% approval on the 29th October and was confirmed on 30th Oct. My 400 shares will become 236 $TDOC shares in November and it will likely become my largest position in the near term.

Some of the leadership at $LVGO will not be staying with Teladoc.

This is unsurprising - we are probably in the midst of one of the greatest opportunities to reshape the healthcare landscape of the last 2 decades. The loss of Jennifer Schneider is perhaps the greatest unexpected loss in my view.

I’ll be intrigued to see what they do with the new SPAC.

Onwards.

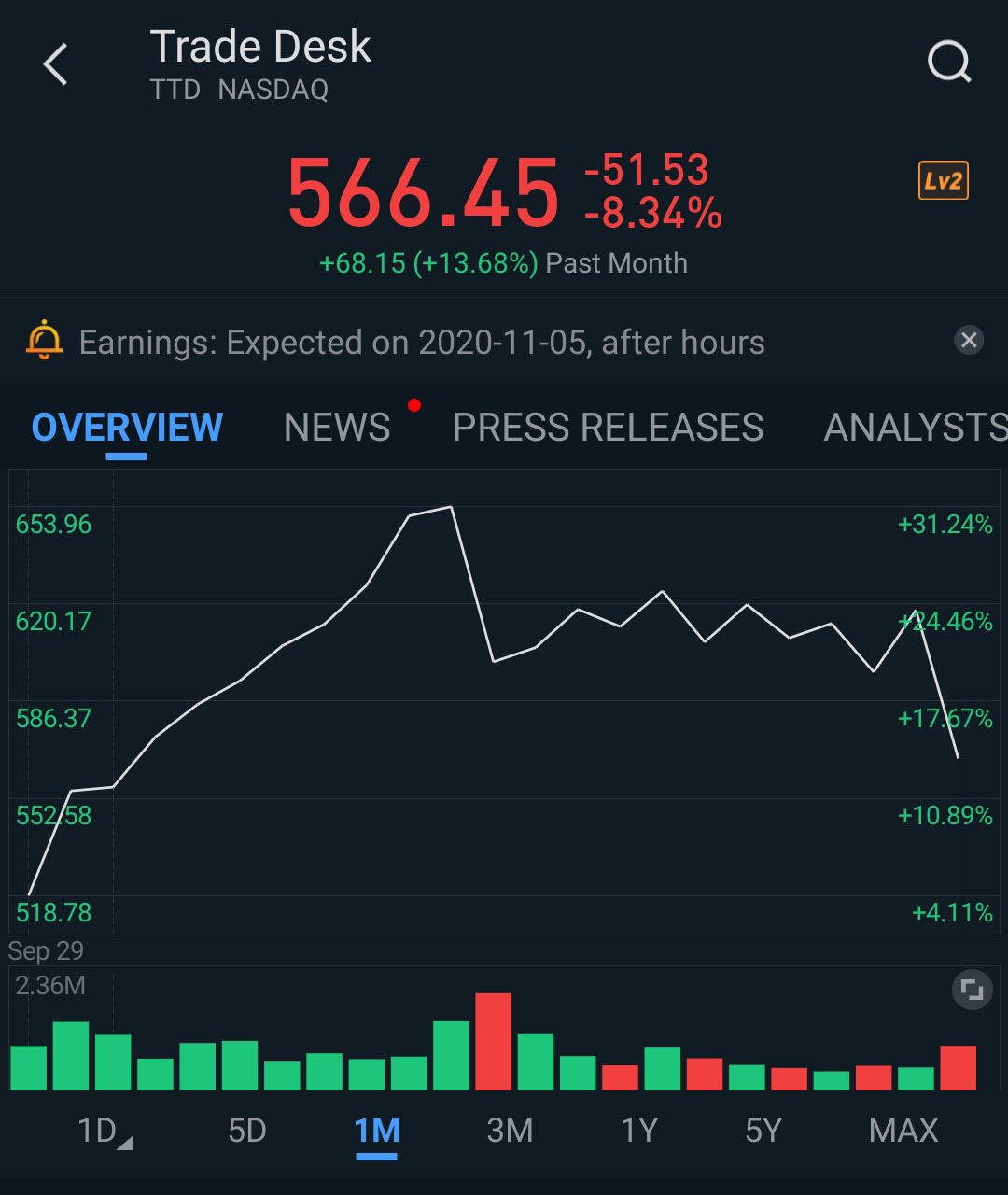

$TTD

I know that digital advertising was making a resurgence ($SNAP, $PINS) but I have no objective explanation why shares hit $670 this month. I think it’s an excellently positioned company with an outstanding CEO, and a long runway, so I’ll hold on for the ride. They will have to do significantly better than the last ER where they got a market pass despite posting negative revenue growth to maintain the current valuation - although there are significant qualitative factors at play as well. The other factor is that $TTD is profitable - a rare thing among software-driven businesses.

$MDB

A flat month for the stock. Some impressive simultaneous cloud capabilities for Atlas.

Mongo keeps chugging along and it’s an easy hold for me.

$AYX

AYX might be my problem child. Last month I mentioned that if I was trying to optimise for the short term, I’d probably drop it. It had a nice boost early in October due to a pre-announcement that ER would be better than guidance. The same announcement contained details of a leadership change that left an unpleasant taste in my mouth.

Dean Stoecker is out as CEO and becomes executive chairman. He has been replaced by Mark Anderson who has sat on the $AYX board for 2 years and has probably been thinking he could do a better job….

I don’t like the way this change has been communicated. I think $AYX has been left flat footed by COVID19 and that there is an urgency to move towards being more cloud native.

This will consume engineering resources and hurt gross margins, but seems like the correct strategic choice. Maybe the board felt Dean was dragging his heels on cloud and left the company exposed? I have no idea, but in any case, the nature of the communication seems unplanned. No previous mention of it on the prior conference call, and I am left thinking that there is more to this than it seems on the surface. My confidence is falling, despite the bump in the stock price. Rumours of an attempted sale do not help.

I sold 25 of my 140 shares (18% of my position) on the bump on the pre-announcement. I may trim my position further depending on my perception of the next ER. $AYX pre-COVID felt like it was executing beautifully but I have significantly less confidence at present.

$TWLO

$TWLO is doing great. The company acquired Segment, posted a great quarter, and are expanding their TAM impressively. It’s an easy hold for me. I trimmed shares back in Nov 2019 due to reduced confidence after they had a sloppy ER, but it feels to me that I should be adding back to my position here - it’s still only 2/3 of intended capital allocation and I have more confidence in $TWLO than in $AYX currently.

$CRWD

An ugly month with no apparent reason for weakness in the stock. But prices are transient and the business continues to innovate at a rapid pace. Stocknovice has put together a comprehensive review of the new products announced at Fal.Con - so there is no need for me to repeat his excellent summary.

$ZS

It has been a fairly unremarkable month for Zscaler. To my eye valuation is stretched vs the operating metrics, but it seems to be back being a market darling. That carries a risk if they slip operationally, as was saw in summer 2019. Tailwinds are there - but they need to execute.

It will be interesting to see what happens if $NET ramps up competition in $ZS’s space, although they currently focus on smaller enterprises.

$ROKU

$ROKU reports next month - given the return of ad-spend and impressive performance of other advertising companies, I suspect it will be good.

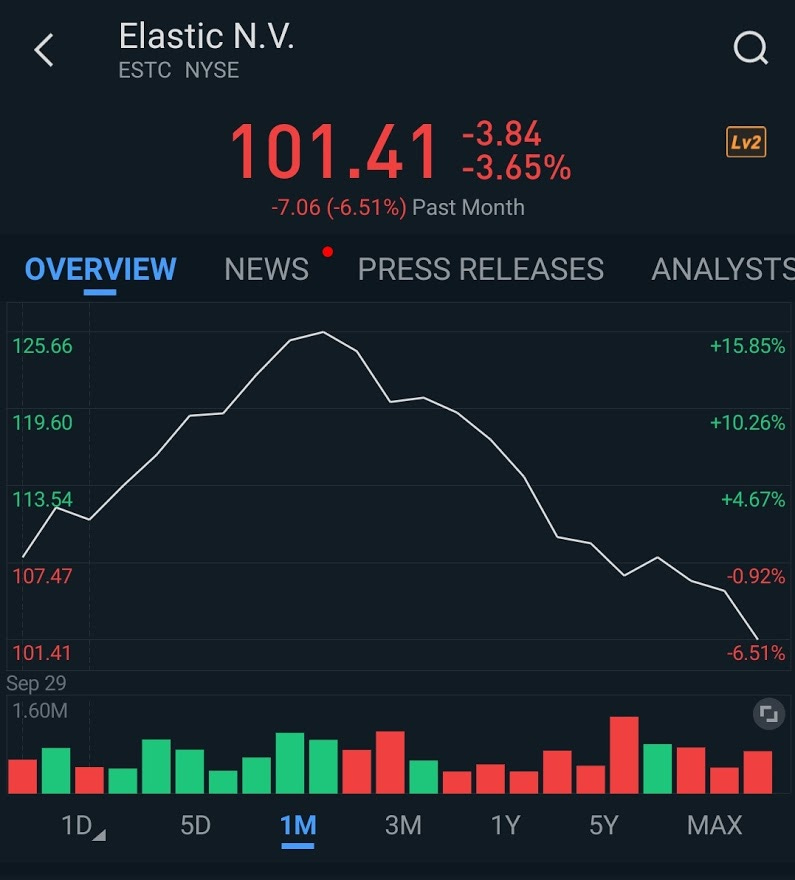

$ESTC

Thesis currently intact, I’m happy holding Elastic.

$NVTA

Invitae have completed the merger with ArcherDX. This should increase the company capability in testing services for disease risk, therapy optimization and personalized cancer monitoring. They have been involved in research that will likely strengthen the the long term demand for their service. Volumes are hopefully continuing to recover this quarter after cratering in Q2. ER is on November 5 in election week.

$BZUN

Patience is hard. $BZUN is on my ignore list until 11.11.20 - I’ll be interested to see how their Single’s Day performance compares to historical.

$API

An ugly month for $API, but there are many good reason I have been taking my time with this one.

$ZM is making some potential inroads into the API-ification of their platform. Investing is largely a game of dealing with probablistic uncertainties, but I think that both companies can coexist and outperform over the long run.

Podcasts I’ve been Listening to

The Loan

Loan balance outstanding: ~ £16.3K

Loan to portfolio value (LTV) rate: 10.4%, down from 11% last month

Final Thoughts

Election drama.

Earnings season.

End of month volatility.

Further lockdowns.

Are all outside of my control, so I try to optimise for what I can control.

Stay safe out there!

Watchlist: $AGCUU, $HAACU, $OAC, $FVRR